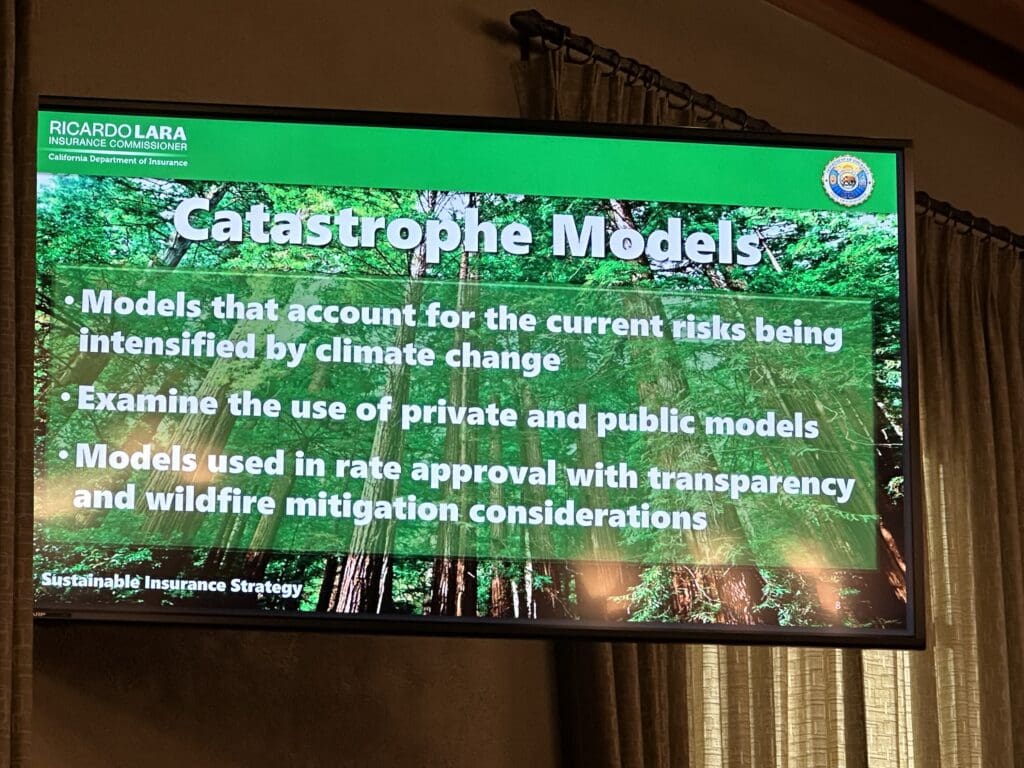

The Safe Community Project participated in a State Assembly hearing on wildfire insurance conducted in Pasadena California on December 13, 2023. Insurance Commissioner Ricardo Lara delivered a presentation during which he laid out the department’s plans for supporting the improvement of wildfire insurance in the state.

According to Commissioner Lara, the State Department of Insurance is the first insurance department (anywhere) with a climate branch. They will host a Global Sustainable Insurance Summit with the United Nations in Spring 2024. The commissioner explained that insurance overall is at a crossroads: There are fewer options and higher costs. This is complicated by outdated regulations and the growing climate threat.

What wasn’t covered were the significant issues impacting homeowners throughout California, and specifically in Southern California where The Safe Community Project operates. The lack of wildfire insurance in Los Angeles has significant impacts on homeowners, particularly in terms of financial stability, property values, and overall risk management. Here are some of the primary effects:

- Increased Financial Vulnerability: Homeowners without wildfire insurance face considerable financial risks. If their properties are damaged or destroyed by wildfires, they are responsible for all repair and rebuilding costs. This can lead to severe financial strain or even bankruptcy for those who cannot afford these expenses out-of-pocket.

- Decreased Property Values: Areas that are highly susceptible to wildfires and where insurance is scarce or prohibitively expensive might see a decrease in property values. Potential buyers may be discouraged from investing in such areas due to the high risk and the difficulty of obtaining insurance.

- Difficulty in Obtaining Mortgages: Lenders often require comprehensive home insurance, including coverage for natural disasters like wildfires, as a condition for a mortgage. Without available or affordable wildfire insurance, homeowners might find it difficult to secure financing or refinance their homes.

- Increased Premiums and Limited Coverage: For those who can obtain wildfire insurance, premiums have been rising, and the scope of coverage has been shrinking. Insurers may impose higher deductibles or cap the amount they will pay for damages. In some cases, policies exclude certain types of fire damage altogether.

- Market for Last-Resort Insurance: As private insurers pull back from high-risk areas, more homeowners may need to rely on California’s FAIR Plan, a last-resort insurance pool that provides basic fire insurance coverage. However, the FAIR Plan is typically more expensive and offers less comprehensive coverage than standard homeowner policies.

- Stress and Uncertainty: Living in a wildfire-prone area without adequate insurance adds a layer of stress and uncertainty. Homeowners may constantly worry about the potential destruction of their property and the financial ruin that could follow.

- Community Impact: The broader community can also suffer. Lack of insurance can lead to slower recovery from wildfires, reducing economic activity and possibly leading to long-term declines in both community resilience and cohesion.

In response to these challenges, some local and state governments, along with insurance regulators, are exploring ways to improve the availability and affordability of wildfire insurance. This includes efforts to promote better land management and building codes to reduce wildfire risks, potentially making it more feasible for insurers to offer coverage. Additionally, there are discussions about state-backed insurance options or publicly funded options. Overall, this is not an issue that is going away, and the tug-of-war between insurance providers and the State is likely to get worse before it gets better.